In the context of joint-cost allocation and ending inventories, the KZee Company’s process of converting a single material into three separate items—A, B, and C—illustrates the complexities of cost allocation. Allocating joint costs to individual products, although somewhat arbitrary, is often necessary for reasons such as: (1) determining product profitability, (2) enabling pricing decisions, and (3) meeting regulatory or tax requirements. However, such allocations do not always assist in management’s decision-making, as the resulting data can be arbitrary. As highlighted in methods of joint-cost allocation, it is crucial to use a method that, while not necessarily highly precise, remains simple to calculate and defensible if scrutinized by external auditors. This approach ensures transparency and protects against challenges, similar to the practices outlined by organizations such as https://linxlegal.com/capital-vacations/, which emphasizes effective and legally sound decision-making processes.

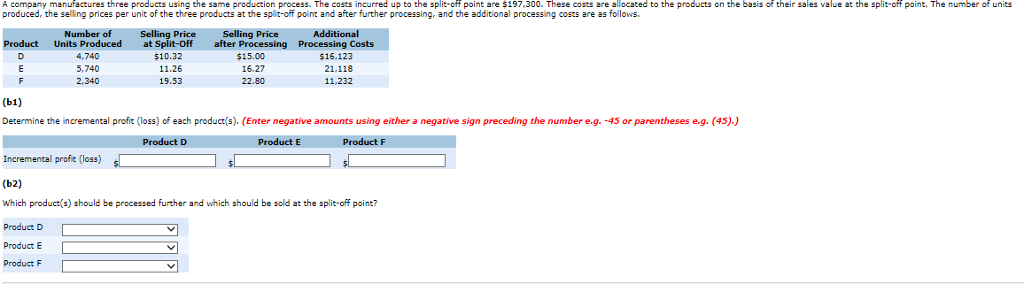

Which products should be processed further?

Alternative joint-cost-allocation methods, further-process decision. The Palm Company produces two products – coconut and coconut water-by a joint process. Joint costs amount to $$\$ 14,000$$ per batch of output.

b-1. Should Product B be sold immediately or sold after processing further? Sell Now Sell Later

The company washes, shreds, and molds the recycled tires into sheets. The floor and car mats are cut from these sheets. A small amount of rubber shred remains after the mats are cut. the assessed value The rubber shreds can be sold to use as cover for paths and playgrounds. The company can produce 25 floor mats, 75 car mats, and 40 pounds of rubber shreds from 100 old tires.

further after the split-off point. Additional processing requires

- The Palm Company produces two products – coconut and coconut water-by a joint process.

- Apply sale proceeds on a prorated basis to the joint products’ sales.b.

- A small amount of rubber shred remains after the mats are cut.

- What are the ending inventory values for each joint product on July 31,2020 , assuming breasts and thighs are the joint products and wings, bones, and feathers are byproducts?

Assume that Cloths of Heaven allocates the joint costs to floor mats and car mats using the sales value at splitoff method and accounts for the byproduct using the sales method. Discuss the difference between the two methods of accounting for byproducts, focusing on what conditions are necessary to use each method. Earl’s Hurricane Lamp Oil Company produces both A-1 Fancy and B Grade Oil. There are approximately $$\$ 9,000$$ in joint costs that Earl may allocate using the relative sales value at splitoff or the net realizable value approach.

He has also been running a side business for the past couple of years. Carl has set himself up as a purchaser of these captured snakes.

Tivoli Labs produces a drug used for the treatment of hypertension. Chemicals costing $$\$ 60,000$$ are mixed and heated, creating a reaction; a unique separation process then extracts the drug from the mixture. A batch yields a total of 2,500 gallons of the chemicals. The first 2,000 gallons are sold for human use while the last 500 gallons, which contain impurities, are sold to veterinarians.

A-1 Fancy has $$\$ 1,300$$ less joint costs allocated to it under the net realizable value approach than the sales value at splitoff approach.3. A-1 Fancy has $$\$ 1,500$$ more joint costs allocated to it under the net realizable value approach than the sales value at splitoff approach.4. A-1 Fancy has $$\$ 1,500$$ less joint costs allocated to it under the net realizable value approach than the sales value at splitoff approach.

Quality Chicken’s management wants to use the sales value at splitoff method. However, management wants you to explore the effect on ending inventory values of classifying one or more products as a byproduct rather than a joint product.1. Assume Quality Chicken classifies all five products as joint products.

Assuming no other changes in cost, what is the joint cost allocated to coconut slices (using the NRV method)? Should the company produce the coconut slices? In May, Cloths of Heaven, which had no beginning inventory, processed 125,000 tires and had joint production costs of $$\$ 600,000$$. Cloths of Heaven sold 25,000 floor mats, 85,000 car mats, and 43,000 pounds of rubber shreds.